The Economic Report of the President

On Monday Dr. Edward Lazear, Chairman of the President’s Council of Economic Advisers, released the Economic Report of the President for 2008.

This traditionally is released a week after the President’s Budget. It describes the state of the U.S. economy, and also discusses in more detail a range of economic policy issues. As the ERP is written by professional economists on the CEA staff, it’s quite substantive. Topics covered this year include the U.S. macroeconomic picture, credit and housing markets, export growth, health care, tax policy, the Nation’s infrastructure, alternative energy, and improving economic statistics.

In addition, Dr. Lazear spoke to reporters yesterday about the ERP, and about the Administration’s economic forecast. Here are some of the most significant quotes from that press briefing. While normally I try to explain our policies, I can’t do better than Eddie has done for himself, so I present his quotes without further ado.

On the economy

CHAIRMAN LAZEAR: Going forward, most forecasters expect the first half of 2008 to have slow, but positive, growth, followed by a pick-up in the latter half of the year. The stimulus package just passed by Congress that will be signed by the President shortly should help ensure against risks in the economy.

This year’s most significant economic events revolved around housing and credit markets. An apparent under-pricing of risk was revealed first in mortgage markets, and later in a variety of credit markets. The President was quick to respond to these issues by focusing on borrowers through programs like FHA Secure, suspension of the tax liability on mortgage write-downs, and HOPE NOW programs. Additionally, the Federal Reserve acted to pump liquidity into the market. Some credit markets have become more stable since the acute tightening that occurred in the summer.

Are we in a recession?

Q: [D]o you think we’re going to go into a recession or are in a recession right now?

CHAIRMAN LAZEAR: The answer is, I don’t think we are in a recession right now, and we are not forecasting a recession. We are forecasting slower growth. There’s no denying that the growth that we had in the fourth quarter of last year was significantly lower than the growth that we had in the third quarter. Now I just remind you that we had similar growth rates in the first quarter of last year, and those similar growth rates were followed by two very strong quarters. So these things are somewhat volatile.

I am not suggesting that we expect that in this quarter we’ll see the same kind of growth that we saw, say, in the third quarter of last year — we’ve had some issues, obviously, in terms of credit tightening, in terms of the housing markets. And that’s the reason why the President was very active in pushing through the stimulus package, which we’re very pleased about. I think we got that in record time. We think that’s insurance against risks on lower economic growth, and we think that will help a good bit. We think it should help immediately, because businesses will build those expectations into their plans, and we expect that will help the economy even in the very near term.

Should people be worried even if we’re not in a recession?

Q: I know you’re not forecasting a recession, but a lot of Americans look at the fourth quarter figures, they look at the stock market, they look at the shrinkage in the job figures in the fourth quarter, and they say, well, I’m worried about it. Are they wrong to be worried about it?

CHAIRMAN LAZEAR: Well, we look at those numbers too, and that was the motivation, of course, behind the stimulus package, because of the concerns out there — and it wasn’t just the public’s concerns, it was our concern that there are some factors that suggest some potential weakness in the economy. We were worried about lower growth, and as a result of that, we decided that it was the right time to act.

We believe that the stimulus package that was voted on last week will be quite effective in ensuring against these downside risks, and we think that they will keep the economy from slipping into lower levels of growth. And again I think that our forecasts are realistic, they’re consistent with what you’re seeing out on the street, as well. I think this is — we’re moving in the right direction.

I should also mention, by the way, that the Federal Reserve has also acted to change their monetary policy stature over the last few weeks, and in a pretty aggressive way, and that will also contribute, we think, to the economic picture.

Is the Administration willing to consider a second stimulus bill?

Q: Congress is planning to advance a second stimulus package in a few weeks. First of all, given the timing, would you even agree that it would be a stimulus package? And whether or not it has a stimulative effect, is the administration willing to consider additional measures?

CHAIRMAN LAZEAR: We think the proposal that we put out a few weeks ago, and it was acted on last week, is the right thing to do. We think 1 percent of GDP is about the right number — it’s slightly higher than 1 percent, but we think that’s an effective stimulus. We think it will have the desired effect. And that was the policy that we thought was appropriate. We still think that policy is appropriate and we’ll stick with that.

Does your forecast assume spillover from the housing problems into other financial markets or economic sectors?

Q: Back in March, the great debate was, will this housing crisis spill over into any other sector, and economists were divided, and of course by August we knew it was spilling into the financial sector. Now, if you pick up the papers you’re reading about corporate debt market seems to be under pressure. Is your forecast assuming no more spillover, or have you actually taken into effect possible spillover into corporate debt and other marketplaces?

CHAIRMAN LAZEAR: Well, when you say “spillover,” I guess I would say that’s still a debatable point. The fact that we saw some distress in other credit markets does not necessarily mean that it was a spillover from the housing market. It could have been, but it could also be a reflection of the same underlying phenomenon. I think most market observers believe that most of what we’ve seen in terms of credit markets reflects the under-pricing of risk that occurred over the past couple of years, that happen to have shown up first in mortgages.

Okay, so it showed up first in subprime. That doesn’t mean that subprime necessarily was the cause of what we saw in other markets. It’s just a reflection of the same forces perhaps showing up there first. And my guess is that will be something that will be debated by academics for the next 10 years to come.

Is it over? You know, who knows whether it’s over. I think the good thing that has happened in credit markets is that many firms have recognized their losses and, in addition to that, they’ve been able to raise capital. I think that’s the most encouraging sign — that firms have suffered some distress and financial markets, no question about it, but after they’ve declared those losses they’ve been able to go out and raise capital and to start again. And that’s what’s most important, I think, going forward.

Debt and the real threat

Monday the President proposed his budget for Fiscal Year 2009. This is the first “e-Budget” – it was transmitted electronically as an official document to the Congress, and was digitally signed by the Executive Clerk.

At a press conference Monday, Senate Budget Committee Chairman Kent Conrad (D-ND) said:

But let me emphasize to you what I see in almost no stories: That is a four-letter word called debt. Nowhere do I see mentioned of what’s going to happen to the debt. It never leaves the administration’s lips. I have never seen it in a single story. I hear a lot of focus on the deficit.

No mention of what happens to the debt.

And I would suggest to you the debt is the threat. Why? Because if you look at what is scheduled to happen in this next year, according to the administration’s own estimates, while the deficit goes up over $400 billion, the debt will go up over $700 billion in one year. The big difference, of course, is Social Security money that is being used to pay other bills. It doesn’t get included in any deficit calculation, but every penny of it gets added to the debt.

The result is, under the Bush administration proposal, they are building a wall of debt. At the end of his first year, the gross debt of the United States stood at $5.8 trillion. We don’t hold him responsible for the first year because he wasn’t in charge the first year. The budget, as you know, is presented by the president outgoing.

If you look at the end of his eight years of responsibility, we see the debt as being over $10.4 trillion. That is almost a doubling of the national debt on his watch. You will recall, he said paying down the debt was a high priority. And we see the debt further escalating to more than $13 trillion by 2013.

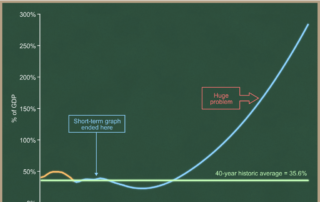

One of Chairman Conrad’s charts says “The Debt is the Threat.” Let’s look at a chart, which purports to show the Federal debt under President Bush’s tenure. Looks pretty bad, no?

")

This is easiest to analyze if we look at the simplest statement made by Chairman Conrad: “That is almost a doubling of the national debt on

I’m going to disprove the statement: “That is almost a doubling of the national debt on his watch.” I don’t dispute the factual accuracy of the numbers, but instead the presentation and the conclusion.

This presentation misleads in three ways.

- nominal $ vs. % of GDP – You can’t compare $1 in 2001 to $1 in 2009, for two reasons. Inflation has made the $1 in 2009 worth less than the $1 in 2001, and economic growth since 2001 increases our economy’s ability to carry the burden of any given amount of government debt. What we care about as an economic matter is not our debt, but our debt burden relative to our ability to support it with our income. As an example, someone with $50K of annual income who takes out a $500K mortgage is borrowing 10X his annual income – that’s nuts. But someone with $1M of annual income who takes out the same $500K mortgage is borrowing 1/2 of his annual income. That’s much more reasonable. Serious analysts look at federal debt over time measured as a share (%) of our national income (GDP), not measures of nominal dollars over time.

- gross debt vs. debt held by the public – (this is the hard part) What we care about is how much the U.S. Government owes to the American public and the rest of the world (meaning how much we owe to those who buy Treasury bonds). This is commonly known as “debt held by the public.” To this amount, the Chairman adds debt that one part of the government owes to another part of the government, to get what budgeteers call “gross federal debt.” If you use funds from your savings account to pay down a credit card, you have decreased your personal “debt held by the public.” For comparison, if you borrow from your savings account and put it into your checking account, and leave in your savings account an IOU from you to you, Chairman Conrad’s metric would say that you have “increased your gross debt.” This is economically meaningless.

- no comparison to the historic average – It’s relevant to compare our federal debt [held by the public] with historic averages, to see if we’re in a lot of debt relative to where we’ve been in the past.

So here’s a new graph, using the same data source (OMB’s Historical Tables), which corrects for these three problems.

Now that we’re looking at a fair analytic presentation, we can draw a few conclusions from this new graph:

- Yes, the federal debt is higher than when the President took office. Debt in 2001 = 35.1% of GDP. Projected debt in 2009 = 37.9% of GDP.

- The claim that the debt is “almost doubling” under this President is absurd. Measured as a share of the economy, it’s about 8% higher than it was when the President took office. (37.9 – 35.1) / 35.1 = 8%

- This debt increase comes in the context of: an inherited recession, a stock market crash, corporate scandals, a terrorist attack, war, and a huge increase in the price of oil.

The President’s budget is merely the first stage in the annual Congressional budgeting process. The next step is for Chairman Conrad, and his House counterpart Chairman John Spratt (D-SC), to each propose his own budget. If their budgets raise taxes more than they increase spending, as was the case last year, then they would show lower debt held by the public than in the President’s budget. But since they so far have not tackled the Social Security challenge, we would still expect those budgets to show significant increases in Chairman Conrad’s preferred metric of “gross debt.”

I want to more fundamentally disagree with Chairman Conrad’s claim that “the debt is the threat.” (He has another chart that says this.) His statement focuses entirely on what has happened to the debt (using a misleading measure) over the past seven years. His focus is: (1) backward-looking, (2) short-term, and (3) focused on debt.

This is trivial compared to what we call “the real fiscal danger”: the projected long-run future growth of federal government spending.

- Where the Chairman’s focus is backward-looking, the real fiscal danger is in the future.

- Where the Chairman’s focus is on the past seven years, we face the real fiscal danger over the next several decades.

- The Chairman focuses on the debt. This is incomplete – our problem is debt driven by projected future spending growth.

To make the first two of these points, let’s recreate the above graph, but I’m going to expand the timeline to cover the next several decade. Same graph, longer timeframe:

Now compare the part of this graph between 2000 and 2010, which is identical to the data in the graph above it, with what happens to the debt beginning in about 2025. On our current long-term policy path, the federal debt would explode beginning in about 20 years. Note that while this chart purports to go out to 2080, we would never make it that far on the light blue line on our current long-term policy path. Financial market pressures would force a change long before our federal debt got to 200 or 250% of GDP.

The real threat is not the additional 2.8% of GDP of debt we have accumulated since the President took office, during a time of recession, war, terrorist attacks, high oil prices, and burst stock market bubbles.

The real threat is that steady and steep upslope in the blue line – the explosion of future debt over the next several decades, if we don’t do something about it. The President has proposed to do something about it, and Congress has failed to act.

Extending unemployment insurance

Some have been arguing that the growth package should extend the availability of unemployment insurance (UI) benefits.

I’d like to cover three points in response:

- Unemployment benefits have never before been extended when the unemployment rate is as low as it is now, or before the economy has been in a recession.

- Extending unemployment benefits will not have a quicker positive effect on GDP growth than tax rebates.

- Extending unemployment insurance benefits encourages some workers to remain unemployed. This could hurt job growth and undo much or all of the near-term positive effects of the House-passed growth package.

Special thanks go to Dr. Edward Lazear and his team at the Council of Economic Advisers for the first and third points. p.s. Eddie is a labor economist.

Unemployment benefits have been extended seven times since the 1950s. Only twice have extended benefits started when the unemployment rate was below 7.0 percent. In both cases, the unemployment rate was above 5.7 percent. The current unemployment rate is 5.0 percent.

Unemployment benefits have never been extended before a recession. Almost all periods of extended benefits occurred after the conclusion of a recession. Twice extensions were initiated 12 months into a recession (1975 and 1982). And of course, our economy is now growing, albeit slowly.

Special Extended Benefit Programs

| Date | Unemployment rate |

| June 1958 | 7.3% |

| April 1961 | 7.0% |

| January 1972 | 5.8% |

| January 1975 | 8.1% |

| September 1982 | 10.1% |

| November 1991 | 7.0% |

| March 2002 | 5.7% |

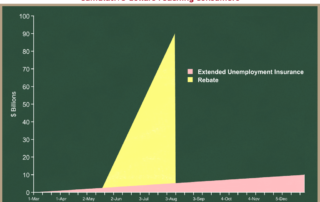

Some (including, unfortunately, the Congressional Budget Office) have blurred the distinction between when UI and rebates begin, and when the actual increase in GDP would occur. The press has repeated the incorrect assertion that “unemployment benefits would affect the economy more rapidly than tax rebates.”

While UI checks would start sooner than rebate checks, the vast majority of the cash out the door, and therefore the GDP effect, would occur much earlier from rebate checks than from extending unemployment insurance.

The logic is quite simple.

- Remember that this is an extension of unemployment insurance, from 26 weeks to 52 weeks. That means you only see the financial effects of the policy change in your 27th week of unemployment.

- The first UI help is felt very quickly, within a few weeks — but it only affects people who are about to exhaust their unemployment benefits. For people who aren’t at 26 weeks yet, they won’t feel the effects till later.

- Hence, the stimulus effect of UI relief begins rapidly for a few, but it grows quite gradually — it gets drawn out over a longer time frame, as more people approach week 27.

- Sending people tax refund checks would start later but would peak quickly instead of being spread out over a longer time. We estimate checks would start about 60 days after enactment, and would be delivered over roughly a 7-week period.

This graph shows the cumulative cash out the door, comparing rebate checks and unemployment insurance. The first thing to notice is the difference in magnitude — UI benefits affect fewer people than broad-based tax rebates, so the total amount of dollars going out the door is much smaller, and therefore the economic benefit is smaller.

But the main point is that, while UI benefits would begin in late March and rebate checks not until about mid-May, the checks are concentrated into about a 7-week window. Once that’s done (say, by the end of June), the whole $100B of rebate checks are out the door and into the economy. The UI benefits grow much more slowly, as people “age into” their extended benefits by hitting the 26-week threshold.

Under current law you’re eligible for 26 weeks of unemployment insurance. The most frequently discussed proposal is to extend that for another 26 weeks, to a full year.

Some find it implausible to suggest that some people would choose to remain unemployed because they don’t want to lose their unemployment insurance. But the numbers don’t lie. Look at the dramatic increase in the percentage of workers who find a job in week 26, right before their UI benefits run out.

In fact, according to two economists from the Clinton Administration, extending UI benefits by 13 weeks increases the duration of the typical spell of unemployment by one to two weeks. (Card and Levine, 2000; Katz and Meyer 1990)

So if you extend UI benefits, you will increase the duration of the typical spell of unemployment. Fewer people will have jobs, and economic growth will be slower. While we’re reticent to put an exact number on this effect, the numbers are significant enough that it could counteract much of the benefits of the House-passed growth package.

Stimulus 2008: a need for speed

The House passed the bipartisan growth bill (aka the “stimulus bill”) yesterday on an overwhelming 385-35 vote. 93% of Democrats and 85% of Republicans voted aye. That vote is a direct result of the cooperation among Speaker Pelosi, Republican Leader Boehner, and Treasury Secretary Hank Paulson on behalf of the President.

The bill now heads to the Senate. Today the President called for quick Senate action:

The temptation is going to be for the Senate to load it up. — We need to get this bill out of the Senate and on my desk so the checks can get in the hands of our consumers and our businesses can be assured of the incentives necessary to make investments.

The Senate Finance Committee is marking up an alternate version of this bill today. There are some in the Senate who have ideas about how they would like to modify the House-passed bill. Various Senators want to:

- add infrastructure spending

- add funds to subsidize housing

- add funds for low-income heating assistance

- extend unemployment insurance

- provide tax rebates to seniors

- eliminate the income cap in the House bill

- change the business provisions to provide relief to firms that do not invest in 2008

There are many lobbying the Senate this week to add additional provisions to this bill. There are two risks: (1) that the bipartisan agreement in the House is derailed by changes made in the Senate; and (2) that the bill becomes a “Christmas tree”, on which everyone wants to hang an ornament, delaying Senate completion.

At the same time, there is a growing chorus calling for the Senate to quickly take up and pass the House-passed bill without amendment.

Treasury Secretary Hank Paulson: “The key here is keeping the deal simple, keeping this simple.” Complexity is our enemy right here. Once you start adding things, it’s a slippery slope, and the process could quickly bog down and screech to a stop here. I don’t think the Senate is going to want to derail this program. And I don’t think the Amreican people are going to be anything but impatient if we don’t enact this bipartisan agreement quickly.”

“Former [Clinton] Treasury Secretary Lawrence Summers testified that the plan — due to pass the House today — was appropriately targeted to achieve its short-term goal. While he said an expansion of unemployment insurance would help spur the economy, ‘there are no possible improvements to the package that would warrant delay.'”

“Former [Clinton] White House Budget Director Alice Rivlin concurred: ‘Quick passage, I believe, is more important than improvements.’ Rivlin urged Congress to resist the temptation to add construction projects to the package. She said that spending would proceed too slowly to give the economy a timely boost and would end up accelerating the deficit.”

“It’s important that this bill not get overloaded. I have a full agenda of things I would like to have in the package, but we have to contain the price,” Pelosi said. “We made a decision, because that’s where we could find our common ground.”

Q: “Senator McConnell is asking to do just that, put your bill on the floor, without any amendments. Should Reid just agree to that, to schedule this without slowing it down with a markup tomorrow?”

Speaker Pelosi: “All I would say is, I would hope that the Senate would take up our bill and pass it, so that this can be as timely as it needs to be.”

Senator McConnell: “In the Democrats’ response to the State of the Union, Gov. Sebelius called on Congress to ‘work together’ quickly on a short-term fix to speed relief to families. Speaker Pelosi and Majority Leader Reid previously called for a plan to be ‘implemented into law without delay.’ The best way to do this is for the Senate to take up and pass the bipartisan compromise crafted by the House and send it directly to the President’s desk — this week. Adding extraneous provisions to this cooperative package will only delay, and possibly derail, relief to America’s famliies and job creators.”

Earmark reform (State of the Union follow-up)

Here’s what the President said last night in the State of the Union about earmarks:

The people’s trust in their government is undermined by congressional earmarks — special interest projects that are often snuck in at the last minute, without discussion or debate. Last year, I asked you to voluntarily cut the number and cost of earmarks in half. I also asked you to stop slipping earmarks into committee reports that never even come to a vote. Unfortunately, neither goal was met. So this time, if you send me an appropriations bill that does not cut the number and cost of earmarks in half, I’ll send it back to you with my veto. (Applause.)

And tomorrow, I will issue an executive order that directs federal agencies to ignore any future earmark that is not voted on by Congress. If these items are truly worth funding, Congress should debate them in the open and hold a public vote. (Applause.)

Here is the Executive Order that the President signed this afternoon.

If you’re interested in perusing earmarks, go to OMB’s excellent earmark website.

You can search bills from 2005. OMB is updating the database for more recent laws.

I suggest you try searching for “museum” in the “Search Earmarks full text” box. I got 273 results.

Here are results of a few other searches:

“genome” – $1.2 M for trout genome mapping at West Virginia University in Morgantown, WV and the Agricultural Research Service in Leetown, WV (in report language)

“dinosaur – $99,000 for environmental improvements for preservation of the dinosaur collection in Pittsburgh, PA. (in the law)

“hockey – $129,000 for the American Hearing Impaired Hockey Association in Chicago, IL (in report language)

“paint” – $1.5 M for a Virtual Reality Spray Paint Simulator System and Training Program at Fakespace Systems in Marshalltown, IA (in report language)

In addition, the huge “omnibus” appropriations bill the President signed at the end of last year contained these two earmarks in report language:

- $846,000 for a Father’s Day Rally Committee

- and $178,600 for New York City’s American Ballet Theater

There are three components to our new policy on earmarks:

- a veto threat if an appropriations bill does not cut the number and cost of earmarks in half from 2008 levels;

- direction to agencies that they should ignore earmarks in report language in future bills; and

- direction to agencies that any “phonemarks” be ignored unless they are put in writing to the Agency. The Agency must then publish the written request on the internet within 30 days. A “phonemark” is when a Member of Congress or Congressional staffer calls an agency and presses for funds to be spent on a particular project, generally within that Member’s district or State.

Veto threat

Using our definition of an earmark, last year’s appropriations bills and the accompanying committee reports contained a total of 11,737 earmarks, which combined spent a total of $16.872 B of taxpayer money. This is the baseline against which we will measure the President’s threat to veto any bill which does not cut both the number and $ amount of earmarks at least in half. (Technical note: The actual comparison with last year will be done on a bill-by-bill basis.)

Last year the President called on the Congress to meet this threshold. This year he’s backing that call up with a veto threat.

Executive action

The new executive order defines an earmark as spending provided by Congress where the purported Congressional direction:

- circumvents otherwise applicable “merit-based or competitive allocation processes;”

- or “specifies the location of the recipient;”

- or “otherwise curtails the ability of the executive branch to manage its statutory and constitutional responsibilities pertaining to the funds allocation process.” (I’ll skip the explanation of this.)

Here’s some general appropriations language in a law:

For necessary expenses of activities authorized by law for the National Oceanic and Atmospheric Administration – $2,856,277,000.

The bill includes a further subdivision of $709 million for the National Marine Fisheries Service, a subdivision of NOAA. So far, so good.

The report language, however, includes the following text:

These funds are distributed as follows:

- Oyster Hatchery Economic Pilot Program, Morgan State University, MD $470,000

- Papahanaumokuakea Marine National Monument Fishery Assistance, HI $6,697,500

- Southern New England Cooperative Research Institute, RI $1,339,500

About 80% of earmarks are of this form they’re in report language, which is not actually part of the bill signed into law by the President. These earmarks are instead incorporated into the “report” that accompanies the bill, more formally known as the “Statement of Managers.” The President focused a spotlight on report language earmarks, because they are never subject to a vote in Congress. If a Member had wanted to amend this bill to strike the $470K of spending for the Morgan State Oyster Hatchery Pilot program, he could not have done so. There’s nothing to amend, since this earmark wasn’t actually in the bill.

But the earmark has a practical effect, even though it’s not part of the law. Why? Imagine you’re the person running the National Marine Fisheries Service. You are not legally required to spend this $470K as the report says you should. But if you don’t, next year when you’re coming to Congress to get your $709M (plus inflation), the Member or staffer whose earmark you ignored might cut your funding. And since report language is generally written by those staffers who actually determine what your top-line number is next year, you have a tremendous incentive to do what they “recommend” in the report.

The President’s executive order now instructs you to ignore those report language earmarks. You have been directed to give money to the Oyster Hatchery Pilot Program only if it merits that funding based on an objective, transparent, and merit-based funding process.

I’ll extract some key language from the Executive Order.

(T)he head of each agency shall ensure that agency decisions to expend funds are based on the text of laws, and in particular, are not based on language in any report of a committee of Congress or any other non-statutory statement or indication of views of the Congress, or a House, committee, Member, officer, or staff thereof.

In other words, follow the words of the law, not what some other person or document claims is the intent of the law.

(T)he head of each agency shall ensure that agency decisions to expend funds for any earmark are based on authorized, transparent, statutory criteria and merit-based decision-making.

Some earmarked projects will still get funding because they qualify on the merits. The process is important here – they will be getting the funds because they are projects that succeed in a merit-based competition based on transparent (public) criteria, not because they have a powerful supporter.

(T)he head of each agency shall “ensure that no oral or written communications concerning earmarks shall supersede statutory criteria, competitive awards, or merit-based decision-making.

An agency shall not consider the views of a house, committee, Member, officer, or staff of Congress to carry out an earmark unless such views are in writing

A “phonemark” is when a Member of Congress or Congressional staffer calls an agency and presses for funds to be spent on a particular project, generally within that Member’s district or State. No more phonemarking. You’ve got to put it in writing.

All written communications from the Congress recommending that funds be expended on an earmark shall be made publicly available on the Internet by the receiving agency, not later than 30 days after receipt of such communication

… and then your letter will be made public. Transparency is key.

Note that the Executive Order has no sunset date – it is now permanent policy. A future President could modify it or repeal it, but they would then be weakening President Bush’s action to limit earmarks.

Economic highlights of the State of the Union address

The President delivers his State of the Union address this evening, beginning just after 9 PM. We typically release “fact sheets” along with the address.

Since the big document is 36 pages long, we also have versions of the different component fact sheets on whitehouse.gov. Here are the economic ones:

We also have separate fact sheets outside the economic lane on National Security, Iraq, the Global War on Terror, Veterans, No Child Left Behind, Education, Stem cell research, Faith-based initiatives, Immigration, and Compassion.

While many inside the Beltway focus on the specific phrasing of key sentences to look for nuances, it’s probably even more important to pay attention to what subjects the President discusses. Those are important signals about his priorities for the upcoming year. This year, roughly the first third of the speech will be dedicated to economic issues. Over the next week or two I’ll drill down and explain the details of what he said on particular topics. Tonight I’ll just point out the broad brush strokes.

Here are a few things you should listen for in tonight’s address:

- The President will push Congress to quickly enact the bipartisan agreement on growth that we announced last Friday. The House plans to vote on it tomorrow, and we’re hoping for a big bipartisan vote. He will ask both the House and Senate to resist the temptation to load up the bill with other provisions. We need speed, and additions could delay or derail it.

- While the bipartisan growth agreement is the most urgent economic need, the most important is making the enacted tax cuts permanent, and preventing taxes from increasing beginning in 2011. He will emphasize that tonight.

- He will talk about the importance of free trade: Free Trade Agreements with Colombia, Panama, and South Korea, and the Doha Round of global trade talks.

- He’ll announce new policy on earmarks – telling Congress that he will veto appropriations bills if they do not cut the number and $ amount of earmarks at least in half. He will also announce that tomorrow he will sign an executive order that directs agencies to ignore future earmarks that are in “report language” which is never voted on by the Congress.

- He’ll talk about health care, and reaffirm his commitment to reform the tax treatment of health insurance. The President’s proposed standard deduction for health insurance would make it more affordable for millions of Americans, and would mean that Americans not fortunate enough to get health insurance through their job would now get the same tax advantage as those who do. More broadly, he’ll emphasize the importance of an approach to health care policy that centers decision-making in individuals and families, rather than in Washington.

- He’ll talk about energy and climate change. In December the Congress passed the President’s energy proposal from last year’s State of the Union to reduce our consumption of oil. This year, he’ll focus more on the power sector, and stress the importance of technology to the three goals of economic growth, energy security, and addressing climate change.

- Hell talk about entitlement reform: Social Security, Medicare, and Medicaid. Many in Congress have expressed their views on the President’s proposed reforms, especially of Social Security, but they have not proposed solutions of their own. He will call on them to put forward their own ideas so we can actually debate how best to make these programs sustainable.

I hope you enjoy the speech. It should be about 45 minutes long.

A bipartisan economic booster shot

Last Friday the President spoke about the need for additional Congressional action on the economy. Outsiders are referring to this as fiscal stimulus. We’ve been calling it a growth package.

There’s a lot to say, so I’m going to break this up into three big parts.

- what the President proposed;

- why the President proposed it; and

- today’s bipartisan agreement, and why we support it.

1. What the President proposed last Friday

Here are the President’s remarks from last Friday. They’re short and well worth reading, and they contain a lot of substantive content.

To put it simply, the President proposed that Congress pull the fiscal policy lever to increase economic growth (GDP) this year. You’ll remember (or not) from your macroeconomics course that there are two basic governmental tools for addressing the short-term economic picture. The Federal Reserve has a monetary policy lever, and the Congress has a fiscal policy lever. The Federal Open Market Committee pulled their lever on Tuesday, by cutting both the federal funds rate and the discount rate by 0.75 percentage points (experts say “75 basis points”). We studiously refrain from commenting on the Fed and its tools.

Last Friday the President described the shape of an effective growth proposal. He did this instead of laying out a detailed proposal, in part at the request of Congressional leaders on both sides of the aisle, to allow them some flexibility in their negotiations. It appears to have worked.

To actually increase GDP in the near term, an effective growth package must be:

- Big enough to move the needle on a $14.5 trillion economy. The President proposed a package that’s 1% of GDP, or about 145 billion dollars in 2008. That’s 50% — 100% bigger than what Congress has been discussing for the past two weeks.

- Immediate. This means (i) Congress should pass legislation immediately. (ii) Policies with immediate macro effects are better than those with lagged effects.

- Based on tax relief. Individuals, families, and businesses will react quickly (and more effectively) if they are deciding how to spend more of their own money. Government bureaucracies react slowly.

- Broad-based. Many were emphasizing “targeted.” In contrast, we think policies should be neutral and distort decisions as little as possible. We have a macroeconomic focus on sectors of the economy, like increasing consumption and business investment. This is in contrast to those who implicitly have a microeconomic focus on particular constituencies in American society. There’s also a difference in philosophical approach, between helping the American economy as a whole, to benefit everyone, and helping those parts/members of the American economy that someone deems to be “most in need of assistance.” (In retrospect, some were also using “targeted” to refer to the income distribution of tax relief. In this respect, we think that the compromise announced today addresses their concerns.)

- And temporary. As a general matter, we prefer long-term policy changes, especially on the tax side. In this case, our policy focus is insuring against drops in GDP growth without significantly raising the national debt. That necessitates short-term and temporary policy changes. (It also dramatically increases the chances of a bipartisan legislative success.)

The President also described a couple of things that move in the wrong direction. To be effective, a growth package must not:

- Raise taxes.

- Waste money on federal spending without an immediate positive effect on GDP growth.

In addition to these principals, the President suggested that a growth package should try to increase consumption (70% of our economy) and business investment (11%). The President said that to be effective, a growth package must:

- Include tax incentives for American businesses to invest (especially small businesses).

- Include “direct and rapid income tax relief” to increase consumer spending.

2. Why our economy needs a booster shot

Here is a memo from the Chairman of the President’s Council of Economic Advisers, Dr. Edward Lazear. It goes into more substantive depth than I will do here.

Our view of where the economy is now

booster shot [boo-ster shot] (n) An additional dose of a vaccine needed to “boost” the immune system.

You don’t get a booster shot when you’re sick. You get it when you’re well, but you’re concerned you might get sick. It’s a preventive measure to reduce the chance that you get sick.

Let’s start with three simple but critically important facts:

- The single most important indicator of a healthy economy is how many people are working. The unemployment rate is now 5.0%. While that’s up quite a bit from 4.7% in the prior month, 5.0% unemployment is still a very good number. Lots of Americans are working, and that’s good. Today’s unemployment rate is below where it was (on average) in each of the last three decades.

- The U.S. economy is growing, albeit slowly. We had a strong 3rd quarter last year (GDP +4.9%). But private sector projections for both Q4 of last year and Q1 of this year fluctuate around +1% (with a big error margin). That’s a significant slowdown, and it’s slower than we would like. (Silly but important reminder: “slowdown” does not equal “recession.” Slowdown means slow growth. Recession means negative growth. Rule of thumb: a “recession” is two successive quarters of negative GDP growth. And for the technicians, yes, the NBER’s definition is actually more complex than this.)

- The President’s economic advisors and most private sector forecasts expect the economy to continue to grow this year, albeit slowly. The most likely scenario is slow GDP growth through the first half of 2008. Most also predict that growth will accelerate somewhat in the second half of the year.

It’s easy to miss these three facts, because much of the press coverage has glossed over them and instead covered the possibility of worse economic scenarios.

Future downside risks provoke economists inside and outside the Administration to recommend an economic booster shot. Most economists raise housing problems and financial markets issues as the greatest near-term threats to continued economic growth. Many also point to the economic drag of expensive oil.

While much of the policy and legislative discussion in the Fall was about housing finance (mortgages), the principal macroeconomic issue is the actual houses themselves. Fast-rising house prices created an incentive for builders to keep putting up new houses beginning in 2003, and inventories built up. When a manufacturer has lots of products in its inventory, it slows down the manufacture of new goods. The same has happened, quite dramatically, in the housing sector. Builders aren’t building because there’s a big supply of unsold houses on the market (with significant regional differences).

As long as housing inventories remain high:

- since supply exceeds demand, prices of new and existing houses will decline (by how much is highly uncertain); and

- builders won’t build many new houses; so

- the residential construction component of GDP will shrink; and therefore

- a shrinking housing sector will cause slower overall economic growth.

These adjustments in the housing sector will take some time. We need to make sure that policy in Washington doesn’t make this problem worse. We are also watching carefully to see whether problems in the housing sector bleed over into consumer spending. This could happen in one of two ways:

- If your home is worth less, you have less overall wealth. The evidence shows that you then spend less (maybe 1 or 2% of the decline in your wealth). This is the “wealth effect.”

- If your home is worth less, you might be less confidence about the economy as a whole, and this might cause you to spend less.

It’s important to understand that the President’s proposal from last Friday was about the U.S. economy as a whole, and his proposal focused on consumer spending (70% of the economy) and business investment (11%). The housing sector needs to adjust, and we can have a greater effect with fiscal policy on consumption and business investment, through the policy direction outlined by the President last Friday.

To summarize:

- Our economy is growing, albeit slowly.

- We think the economy will continue to grow, albeit slowly. We are not predicting a downturn.

- There are risks to that growth projection, especially from housing, the financial markets, and high oil prices.

- The President proposed that Congress quickly enact legislation to address these risks.

3. Today’s bipartisan agreement, and why we support it.

A short while ago House Speaker Nancy Pelosi (D-CA), House Republican Leader John Boehner (R-OH), and Treasury Secretary Hank Paulson announced their agreement on a growth package. The Speaker said she intends rapid legislative action in the House.

Here’s a useful summary, followed by our evaluation of how this agreement fits with the principles the President offered last Friday.

House Bipartisan Leadership Growth Plan Agreement

What it does:

- Part I: Personal Tax Relief ($103 B)

- Cut the 10% tax rate in 2008 to 0% for the first $6,000 (individuals)/$12,000 (couples) of taxable income

- Maximum rebate: $600 (individuals)/$1200 (couples)

- Minimum (refundable) rebate check: $300 (individuals)/$600 (couples)

- Eligible if earned income > $3,000 (subject to income limits below)

- Rebate phases up from $300 to $600 for those with taxable incomes ranging from $3,000 to $6,000

- Additional refundable tax credit of $300 per child for those who otherwise receive a rebate

- Full rebates/credits are available to those with adjusted gross income (AGI) < $75 K (individuals)/$150 K (couples)

- Total rebate (including child credit) phases out above $75K/$150K (by 5% of AGI above those levels, until eliminated)

- Relief provided via rebate checks sent ASAP after enactment (estimated starting date = 60 days later)

- Examples:

- Single parent with two children, earned income of $4,000 (has no current income tax liability).

- Individual rebate = $300

- Child tax credit = $600

- Single parent with two children, AGI = $38,000, taking standard deduction.

- Individual rebate = $450

- Child tax credit = $600

- Married couple with two children, AGI = $48,000, taking standard deduction.

- Individual rebate = $800

- Child tax credit = $600

- Married couple with two children, AGI = $80,000 (assuming tax liability greater than $1,200).

- Individual rebate = $1,200

- Child tax credit = $600

- Single parent with two children, earned income of $4,000 (has no current income tax liability).

- Part II: Business Investment incentives (~$50 B)

- Accelerated bonus depreciation of 50% in 2008

- Increased expensing for small business (Section 179 limit raised from $125 K to $250K)

The agreement would also increase the conforming loan limits for Freddie Mac, Fannie Mae, and the Federal Housing Administration.

Why it is good:

- Effective: The package addresses the two major components identified by the President as essential to promoting near-term growth: boosting consumer spending and business investment.

- Timely: The personal tax relief will begin to stimulate consumer spending and additional economic growth within about 60 days of enactment. The business incentives will spur investment throughout 2008.

- Temporary: The package will provide immediate relief to the economy without turning away from policies to promote long-term growth and to balance the Federal budget.

- Rewards Work: Individuals must have earned income to receive the $300 rebate check.

- Broad-based: Rebates will reach 117 million households.

- Neutral: The package allows individuals and businesses to decide how best to use the relief provided.

What it does not do:

- The package does not raise taxes.

- The package is not a collection of spending programs; it does not include any government outlays beyond the minimum rebate check and refundable child tax credit.

- The package does not contain wasteful provisions that would spend money slowly, failing to meet near-term economic objectives.

- The package does not contain lender bailout provisions that would interfere with ongoing and necessary corrections in the housing sector.

I want to return to the criteria the President laid out last Friday, to see how the bipartisan agreement matches up.

- Big The President proposed 1% of GDP, or about $145 B. This package is about $153 B.

- Immediate We got a bipartisan agreement in the House even faster than we expected, thanks to the excellent work and leadership of Secretary Paulson, Speaker Pelosi, and Leader Boehner. We hope for quick legislative action, and similar bipartisan support in the Senate. TBDWe anticipate advance refund checks could start being delivered about 60 days after the President signs the bill into law. TBD

- Based on tax relief The entire package is done through tax relief, excepting one mortgage-related provision (that does not affect spending). The refundable aspects of the tax relief technically count as spending. But the other spending items (which we opposed) are all excluded from this agreement.

- Broad-based It is very important to us that the government not pick particular constituencies as more “deserving” of tax relief. The agreement largely meets that test.

- Temporary Every provision in this bill is effective only for 2008.

- Don’t raise taxes.

- Don’t waste money on federal spending without an immediate positive effect on GDP growth.

You can see why the President is strongly supporting this bipartisan agreement. He said a short while ago, “Because the country needs this boost to the economy now, I urge the House, and the Senate, to enact this economic growth agreement into law as soon as possible.” We have an opportunity to come together, and take the swift, decisive action our economy urgently needs.

{kind=link}

{kind=link}

{kind=link}

Health insurance for poor kids

This past weekend the President signed a short-term extension of a program that finances health insurance for children, called SCHIP: the State Children’s Health Insurance Program. We expect the Congress today will send the President H.R. 976, a bill that reauthorizes SCHIP for five years. The President has said he will veto this bill, and we expect the House will attempt to override the veto.

This debate is generating much heat and little light. Our critics claim that, because he opposes this bill, the President doesn’t want to help poor kids.

That is of course untrue, so let’s look at where we agree with this bill, where we disagree, and what we would do differently.

Here’s where we agree.

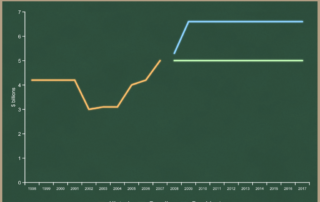

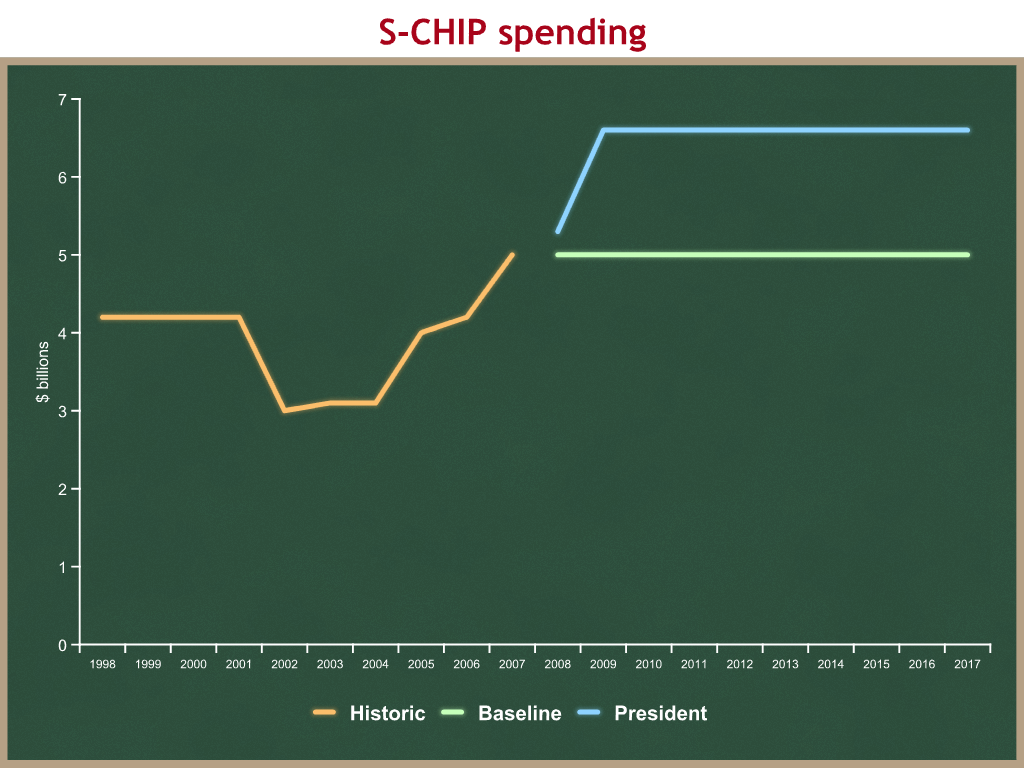

- We agree with the Congress that SCHIP should provide sufficient funding to States to finance health insurance for poor children. The President’s budget would increase total SCHIP spending over the next five years by 20%, from $25 B in total to about $30 B. The gold line below is past funding. The green line is a straight extension of current law (called the baseline). The light blue line is the President’s proposal. (Note that the light blue line shows an even bigger 30% increase, because some States have funds they have not yet spent.)

- We agree with the Congress that there should be no funding gap while we attempt to resolve our differences. At the same time we’re “aggressively debating” the right long-term solution, it’s encouraging that we have agreed not to allow funding to lapse in the short run. Last weekend the President signed a bill that will keep funding going to States through mid-November.

Here’s where we disagree.

- We think the “C” in SCHIP stands for “children.” Over the past several years, adults have been added to SCHIP. Some were parents of kids with health insurance, others were adults without children. We were responsible for some of those additions, as we approved State waiver requests. We made a policy shift this year, based in part on further input from the Congress, and we’re now returning SCHIP to its original purpose. Over the next few years, our policy will return SCHIP to a kids-only program. States that are now covering adults will have to move them onto Medicaid or a State program. While the advocates for HR 976 argue they share this goal, the bill doesn’t match the rhetoric – it lets adults in some states back into SCHIP. And in six States (IL, NJ, MI, RI, NM, and MN), more than half of their projected SCHIP expenditures this year are for adults. We think this is the wrong direction for a program that should be about children.

- We think SCHIP should be about helping poor kids. This bill also raises taxes to subsidize health insurance for some middle-income kids. New York wants to use Federal dollars to cover kids who are clearly not poor: for a family of four, they would like to use Federal tax dollars to pay 65% of health insurance costs for a family of four with income as high as $82,600. (We measure this in terms of a multiple of the “poverty line” – NY wants to cover kids up to 400% of poverty.)

This is a fundamental philosophical difference – should we collect more taxes to subsidize those in the middle class, or fewer taxes and subsidize only the poor? The President wants to focus Federal tax dollars on helping kids in families with incomes below twice the poverty line. Note that in the current debate, they count as “poor” kids.

We created a lot of heat by sending a letter from the head of the SCHIP program, Dennis Smith, to State Medicaid Directors. Basically, Dennis’ letter says to States, “You can’t expand your program to non-poor kids until you’ve demonstrated that at least 95% of poor kids in your State have coverage.” Amazingly, this simple insistence that we help poor kids first is considered controversial.

New York has announced they’re going to sue CMS. Should a childless Kansas couple with $50K of income pay higher taxes to subsidize health insurance for a New York family with two kids and $80K of income, when the Kansas family may be having trouble affording health insurance for themselves? We think not.

Congressional advocates for HR 976 argue that we have been misrepresenting HR 976 – they argue that the bill does not provide extra federal funding for all kids up to 400% of poverty. To be clear, it does not, nor have we claimed that it does. The bill does, however, provide extra federal funds to subsidize some kids who are not poor. Under HR 976:

-

- In New York, kids up to 400% of poverty would be eligible and the State would be paid extra to enroll these kids. For a family of four, this is $82,600 of annual income.

- In New Jersey, kids up to 350% of poverty would be eligible and the State would be paid extra to enroll these kids. For a family of four, this is just over $72,000.

- In all other States, kids up to 300% of poverty would be eligible and the State would be paid extra to enroll these kids. For a family of four, this is just over $62,000.

- We think the goal should be maximizing the number of kids with health insurance, not maximizing the number of kids enrolled in government health insurance programs. The President’s priority is to help kids without health insurance afford the purchase of private health insurance. Unfortunately, this bill would encourage families to drop the private health insurance they have now for their kids, and instead substitute low-premium government-provided health insurance. This is called “crowd out,” and it’s both undesirable and a tremendously inefficient use of taxpayer dollars. If a family drops a kid’s privately-purchased coverage, and substitutes health insurance financed by the taxpayer through the government, then you haven’t reduced the number of uninsured kids. Our numbers suggest that, under HR 976, one in three people newly enrolled in SCHIP would be people who dropped their current health insurance to get something from the government (mostly) for free. The Congressional Budget Office estimates that under HR 976, 2 million of the 5.8 million new people enrolled in government health plans would drop private insurance to enroll.

- We don’t think you should raise taxes to pay for more spending. And tobacco taxes are regressive – they fall hardest on low-income people.

- We think this bill is fiscally irresponsible, because it creates an unfunded and unsustainable set of promises. As you can see from the graph below, HR 976 would increase spending by 121% over five years. But it would then cut spending 65 percent over two years, to below where it is now.

This is clearly unrealistic. Once the expectation is created among individuals and the States for $14 B / year of spending, the likelihood that the Congress would actually allow a 65% funding cut is near zero. In reality, the actual projected spending probably looks like this.

The bill doesn’t pay for this increased spending in the “out years,” because technically it assumes the big cut after 2012. So it raises taxes by “only” $73 B over ten years, when a more realistic long-term spending assumption would require even higher taxes to offset the increased spending. (Astute observers will notice that the historic spending on these two graphs is different from the first graph. That’s the difference between when money is allocated to the States, and when cash actually is spent on health insurance. In the budgeting world, the first is called budget authority, and the second outlays.)

- We believe this is a step toward a government-run system for all Americans. The President has made clear that he believes this is the wrong direction. He prefers a system in which the patient (and consumer) is at the center of decisions about his own health care. Moving toward more government financing, and more people in health plans chosen by the government, means less control for the patient, and more decisions made in Washington and in State capitals. This is bad.

In contrast, the President has worked with the Congress to enact changes that give patients more choices and more control over their health care (competing private Medicare drug plans, competing Medicare Advantage insurance plans, Health Savings Accounts), and he has proposed a host of other changes that move in the same direction (especially Association Health Plans, allowing people to buy insurance across state lines, and changes to the tax code, described below).

- We believe we have a better way to help more people afford private health insurance, at less cost to the taxpayer. The President proposed a change to the tax code which would create a “Standard Deduction for Health Insurance.” When combined with the President’s SCHIP proposal, this Standard Deduction would result in significantly more people being able to afford (and buying) private health insurance. His proposals would combine direct assistance (through SCHIP) for poor kids, and a voluntary tax incentive for most everyone else. I’ll try to describe that in more detail in a future note.

One House Democratic leader said that a Presidential veto would be a “political victory” for the Democrats. We’re looking for those who are instead more interested in finding common ground with us on a responsible policy to help poor kids get health insurance, and to making health insurance more affordable for all working Americans.

Update: The President vetoed the bill on October 3, 2007. The House tried to get 2/3 to override and failed, 273-156.

Subprime mortgages, part 2

This is part two (of two) of your crash course on problems and solutions in the mortgage markets. Here’s part one. There is also a great op-ed on the financial market impacts of these mortgage market problems. It ran in today’s Financial Times, and was coauthored by two Administration officials: Treasury Undersecretary for International Affairs Dave McCormick, and Treasury Undersecretary for Domestic Finance Bob Steel.

In addition to the policies the President proposed to help some homeowners struggling with their mortgages, he also discussed several important policy changes intended to reduce the chance that these problems recur. We call the whole package of policies the HOPE program: HomeOwner Protection Effort.

There’s been enormous innovation in the mortgage sector. This has made credit more affordable and more available to millions of people. The vast majority of them will be fine. The public debate will focus on those who are not.

Before we discuss solutions, let’s make sure we understand why the subprime problems happened. I discussed this in the last note, but want to supplement that description here.

There are two important causes:

- Mortgage innovation resulted in some borrowers getting in over their head. Some borrowers didn’t understand what they were buying when they got an ARM with a low teaser rate. In some cases, lenders didn’t provide adequate disclosure. Other borrowers got the disclosure they needed, but didn’t understand it. In still other cases, borrowers didn’t accurately disclose their financial condition. Many borrowers got mortgages that they would be able to refinance only if housing prices continued to appreciate. Some of them knew this, others did not. After the fact, its hard to tell who fits into which category.

- There are also broader financial market practices underlying the recent problems. The growth of subprime markets was partly driven by investors awash in capital, searching for yield and relying on credit ratings and new securitization practices.

I’ll group the policy answers into the same two categories. The first could be called homeowner protection. In another context, it might be called consumer protection.

- The financial regulators have issued new guidelines to enhance disclosure when you buy a mortgage. The Federal Reserve expects to propose a new disclosure rule by the end of the year. Like the Mulroney sticker on a new car window, better disclosure up front means more well-informed buyers. In particular, a borrower needs to know about potential future increases in monthly mortgage payments.

- These regulators are also tightening mortgage lending standards. They have published new guidance to subprime lenders. The most important element of this guidance is that a lender should determine that you qualify under the higher interest rates expected after the reset, and not just at the low introductory teaser rate. And the Fed is working on a rule to ban certain egregious mortgage products and lending practices.

There’s a certain amount of unavoidable tradeoff here: tighter lending standards mean fewer loans will be issued. Fewer loans makes it harder for existing borrowers to refinance (bad), but it reduces the likelihood that new borrowers will get into trouble (good). It’s a balancing act.

As we work through subprime difficulties over the next year+, it’s important to remember that expanded credit and financial innovation are generally good things. Innovation in credit markets has allowed lenders to diversify their risk and expand credit to many who in the past would never have been able to borrow. This has meant higher homeownership rates, more poor people owning cars, and more people being able to afford college. Expanded access to credit, accurately scored and provided by responsible lenders to well-informed borrowers, helps expand access to financial opportunities to a broader swath of the American public. Credit is not and should not be just for the rich. Clearly, however, some lenders behaved inappropriately in the subprime market, so some tightening of lending standards makes sense.

- We’re also dusting off RESPA reform, aka the Real Estate Settlement Procedures Act. This fall, we will propose RESPA reforms that would promote comparative shopping by consumers for the best loan terms, provide clearer disclosures, limit settlement cost increases, and require mortgage brokers to fully disclose their fees and closing costs.

- We’re promoting financial education and counseling. The President will be creating a council on financial literacy, and we’ve got money in our budget for groups like NeighborWorks that help borrowers understand their financial options.

In addition, we’re looking at a couple of financial market issues. We’re using a group called the President’s Working Group on Financial Markets, chaired by Treasury Secretary Hank Paulson, to examine some of the broader market issues underlying recent mortgage problems. One thing this group will do is review policy issues surrounding credit rating agencies. The Working Group includes Fed Chairman Ben Bernanke, SEC Chairman Chris Cox, and Commodity Futures Trading Commission Acting Chairman Walt Lukken.

Finally, Dave and Bob write about some international steps that Secretary Paulson is taking with his counterparts in other leading industrialized nations. Please see the op-ed for more on this topic.

Subprime mortgages

In the Rose Garden last Friday, the President proposed policy changes to address problems in the subprime mortgage market. Here are his remarks and a fact sheet. I’m going to do this in three parts: (1) give a few definitions for those who are new to the housing finance world; (2) define the problem; and (3) explain the President’s new proposals.

Let’s begin with a few definitions:

- A subprime mortgage is one in which there is more risk to the lender than from a prime borrower. A subprime mortgage may be to a borrower with poor credit, or for a loan with little or no down payment, no mortgage insurance, or little or no documentation of income. Note that subprime does not necessarily mean low income. Subprime mortgages are just as high a percentage of big loans (jumbos, in which the loan amount is >$417K) as of smaller loans.

- An ARM is an adjustable rate mortgage. This is in contrast to a fixed rate mortgage. In an ARM, the interest rate changes over time.

- A 2/28 mortgage is a specific type of subprime ARM. Typically, you pay a low fixed teaser interest rate for two years (and often no principal). In month 25, your interest rate resets to a (much) higher rate. Your monthly mortgage payments jump, in some cases quite dramatically. And your interest rate continues to reset every six months after the first reset. A 2/28 mortgage (or its cousin, a 3/27) is one in which the interest rate starts low, then jumps after two years. In most cases, you put little or no money down, and you’re hoping that the value of the home will appreciate significantly during those first two years. If it does, you can probably refinance with an affordable fixed rate, since you now have equity in the home. But if the house does not appreciate in value (or if it depreciates), you’re stuck with much higher monthly payments. Problem: In some cases, people bought such a mortgage where they realistically would never be able to afford the higher monthly payments after the reset. In some markets housing prices have declined over the past two years. These people are having trouble making their higher (post-teaser) monthly mortgage payments. So, for instance, imagine a $200,000 30-year subprime ARM, which has a 7% teaser rate for 2 years, followed by a steadily climbing rate beginning in year 3. If market interest rates rise, your monthly mortgage payments could increase from $1,531 in years one and two, to $1,939 in year three, to $2,370 by year five.

- Refinancing is when you get a new loan (presumably, with a better payment stream) that replaces the original loan. Modification is when your lender helps you out by reducing the interest rate, or forgiving a portion of the loan, or allowing you to skip payments for a while, or allowing you to defer payments to the back end of the loan. Foreclosure is when the lender gives up on the mortgage and takes your house.

Now here’s your crash course in the subprime problem. In 2005, 2006, and the first half of 2007:

- interest rates were low,

- home prices were appreciating,

- the economy was strong, and

- financial innovation had increased the ability of lenders to raise capital from markets, and to provide credit to borrowers.

There was also a proliferation of adjustable rate mortgages, especially subprime ARMs. Much of what is happening now is driven simply by the calendar. Earlier this year, the first big chunk of subprime ARMs issued in early 2005 hit their two-year interest rate reset. Those homeowners suddenly saw their monthly mortgage payments jump. At the same time, interest rates were rising, and housing prices were depreciating in some areas (especially California, Arizona, and Florida). Nationwide, the economy outside of the housing and financial sectors is strong, but in some areas of the country (such as Michigan and Ohio) the regional economies are still slow. These factors combined to increase the number of mortgage holders who were facing financial pressure. In the extreme case, there was an increase in the number of foreclosures. You can see from this graph that resets will continue through the first quarter of 2009. Again, this is driven by the calendar. It means this problem will be with us for a while, as more homeowners will face financial pressures as the mortgages issued in 2006 and the first half of 2007 reset. Remember that when you’re still hearing about housing all next year. ") Not everyone who faces an interest rate reset loses their home. In fact, we expect more than half of them to either refinance, or just tolerate (and pay) the higher monthly payments. On TV you can now see ads for lending firms that are offering to help you refinance before your reset hits. Some will be on the margin — they can’t quite afford their mortgage, but with a little flexibility from their lender, or a little help from the government, they can stay current. The President’s new proposals fall into this category. Others bought homes they just couldn’t afford. Some of these people knew their payments would increase, and planned for it (imagine a married grad student planning to graduate before his rate resets). Others were betting that future increases in the value of the home would give them enough equity to refinance when their reset hit. Still others didn’t know, or were bamboozled by whoever sold them the loan. For whatever reason, some of these people still have no equity in the home, and they simply can’t afford the higher monthly payments. These are the subprime borrowers most likely to face foreclosure. Subprime mortgages, and the financial securities derived from them, are also a principal causal factor in recent problems in the financial markets. Last Friday, the President announced three new initiatives aimed at helping homeowners who are struggling to meet their mortgage payments:

Not everyone who faces an interest rate reset loses their home. In fact, we expect more than half of them to either refinance, or just tolerate (and pay) the higher monthly payments. On TV you can now see ads for lending firms that are offering to help you refinance before your reset hits. Some will be on the margin — they can’t quite afford their mortgage, but with a little flexibility from their lender, or a little help from the government, they can stay current. The President’s new proposals fall into this category. Others bought homes they just couldn’t afford. Some of these people knew their payments would increase, and planned for it (imagine a married grad student planning to graduate before his rate resets). Others were betting that future increases in the value of the home would give them enough equity to refinance when their reset hit. Still others didn’t know, or were bamboozled by whoever sold them the loan. For whatever reason, some of these people still have no equity in the home, and they simply can’t afford the higher monthly payments. These are the subprime borrowers most likely to face foreclosure. Subprime mortgages, and the financial securities derived from them, are also a principal causal factor in recent problems in the financial markets. Last Friday, the President announced three new initiatives aimed at helping homeowners who are struggling to meet their mortgage payments:

- We’re expanding the availability of mortgage insurance sold by the Federal Housing Administration (FHA). You have to meet certain credit requirements to buy mortgage insurance from FHA. One of those requirements is that you have to be current on your mortgage payments. (Current means you’re not behind.) Our new initiative would allow you to buy FHA insurance even if you’re not current, as long as the reason you were late was because of an interest rate reset (I’ll explain this more in a bit.) You also still need to meet FHA’s other credit tests. This mortgage refinancing product is designed to help homeowners who recently saw their monthly payments jump, and are now having trouble making those payments. We don’t need to change the law to do this — FHA is doing it administratively. We call this FHASecure. The President also renewed his call on Congress to pass our FHA modernization proposal. The President proposed this over a year ago. The House passed a close version of it with more than 400 votes last year. So far, neither the House nor the Senate has acted this year. The proposal would allow FHA to offer lower down payment requirements, to insure bigger loans, and to allow FHA to price premiums based on risk. These reforms would help more first-time homebuyers and those with low and moderate incomes, and would give those refinancing their homes more mortgage insurance options.

- The President proposed changing the tax code. We would make cancellation of mortgage debt a non-taxable event.

Example: You bought a $200,000 house two years ago with no down payment. Housing prices in your area have declined dramatically, so your house is now worth only $180,000. Your monthly mortgage payments just jumped, and you and your lender agree that you won’t be able to make your mortgage payments going forward. Since a lender typically loses 20% (rule of thumb) when they foreclose, your lender wants to modify your loan to work something out with you, so you can keep your house, and your lender will lose less than 20% of the loan. Let’s say your lender decides to forgive (“cancel”) $20,000 of your $200,000 mortgage, so now your $180,000 home is paired with a $180,000 mortgage (I’m oversimplifying.) Under current law, the $20K of debt your lender “canceled” counts as taxable income. If you’re in the 25% income tax bracket, you have to pay $5,000 of taxes on that. Since you”re only in this position because you”re strapped for cash, the one thing you can’t afford is to pay $5,000 more taxes. This makes it less likely that you and your lender will be able to work out the loan modification in the first place, and makes it more likely that you’ll face foreclosure. Conceptually, the tax code now recognizes the decline in your debt, but ignores the decline in the value of the corresponding asset. The President is joining Senator Stabenow (D-MI) and Senator Voinovich (R-OH) in proposing to exempt this cancellation of mortgage debt from taxation. We would have this be a temporary change, and apply only to your primary residence. In the House, Rep. Rob Andrews (D-NJ) and Ron Lewis (R-KY) have proposed a similar change. - Treasury and HUD are reaching out to interested parties in the home financing world — lenders, loan servicers, FHA, the Government-Sponsored Enterprises (Fannie Mae and Freddie Mac), and especially community organizations like NeighborWorks that help struggling homeowners in these situations. They’re looking for synergies to expand mortgage financing options, to educate homeowners about those options, and to match homeowners with lenders.

In addition to the above proposals, last Friday the President discussed policy changes that will reduce the chance that these problems recur in the future. I will describe those soon.